JHVEPhoto

Marsh & McLennan Companies (NYSE:MMC) is a leading professional service provider for risk, strategy, and human capital. With annual revenues exceeding $20 billion, Marsh & McLennan has consistently achieved high-single-digit revenue growth organically, along with a consistent margin expansion in recent years. Their business growth demonstrates remarkable resilience across various economic cycles, and a strategic shift towards higher-growth areas has enabled them to accelerate their organic revenue growth.

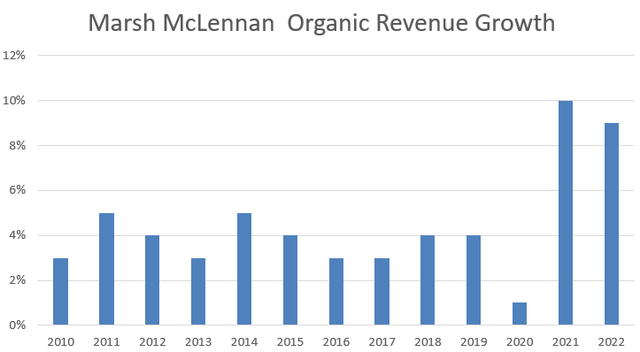

Resilient Growth Across Different Cycles

Since FY10, Marsh & McLennan has never experienced negative organic revenue growth. Even during the pandemic period, their organic revenue increased by 1% in FY20 and rebounded to 10% in FY21.

MMC 10Ks

The key reasons for their business resilience are as follows:

Mandatory Nature of Risk and Insurance Services Spending: Risk and Insurance Services account for more than 60% of Marsh & McLennan’s total revenue. These services encompass risk advice, risk transfer, and risk control and mitigation solutions. During economic downturns, it is unlikely that financial institutions would reduce their budgets for risk management and mitigation solutions. In other words, these services are indispensable for Marsh & McLennan’s customers, regardless of the economic environment.

Product Innovation: Marsh & McLennan has been expanding its service offerings to address the increasing types of risks associated with financial institutions. For instance, there is a growing demand for services related to ESG, cybersecurity, and retirement planning in recent years. Marsh & McLennan has responded by introducing new services in these areas. These additions not only broaden their service range but also create additional revenue streams for the company.

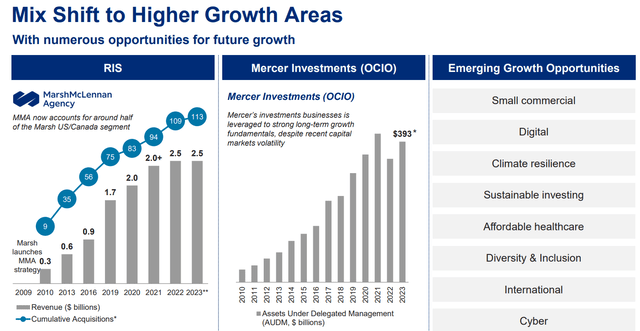

Mix Shift More to Growth Areas

In recent years, Marsh & McLennan has intentionally redirected its focus towards growth areas. They have identified several emerging growth sectors, including digital, climate, sustainability, and cybersecurity, among others.

MMC 2023 Investor’s Presentation

Marsh & McLennan’s management has demonstrated a dedicated commitment to rebalancing their business portfolio towards high-growth sectors. They have been actively attracting talent to these new operations and strategically leveraging acquisitions to broaden their service offerings. I believe that these concerted efforts have the potential to significantly boost their revenue growth in the coming years, and I view these new services as part of their ongoing corporate innovation initiatives. Moreover, it’s worth noting that these new services are likely to carry higher profit margins compared to traditional services, which can further contribute to margin expansion through this mix shift.

Active Cost Management

Marsh & McLennan is effectively managing its costs and has implemented a cost restructuring program. In Q2 FY23, they anticipate achieving total savings of approximately $300 million by FY24, having already realized approximately $200 million in FY23. These cost-saving initiatives encompass reorganization in underperforming units, lease exits, and the streamlining of technology platforms. It’s worth noting that Marsh & McLennan has a history of successfully implementing such cost-saving programs in the past, demonstrating their commitment to maintaining high efficiency.

As a result of these cost-saving efforts and business growth, Marsh & McLennan has seen a remarkable margin expansion of 1,210 basis points from FY10 to their FY23 guidance of 25.6%. This history of margin expansion is indeed noteworthy.

Financials and Outlook

As of Q2 FY23, with $1.2 billion in cash and $12.6 billion in debts, Marsh & McLennan’s estimated gross leverage stands at 2.1x in my model. Given their business resilience, I believe this level of debt leverage is entirely manageable.

Marsh & McLennan’s capital deployment plan for FY23 includes allocating $4 billion across dividends, share buybacks, and acquisitions. Over the past five years combined, they have generated over $15 billion in cash from operations. During this period, they allocated $4.8 billion for dividends, $4.2 billion for share buybacks, and $8.5 billion for acquisitions. Notably, historical data suggests that acquisitions have contributed 1% to 3% to their topline growth. I anticipate that Marsh & McLennan will continue to follow this capital allocation strategy, directing funds towards dividends, buybacks, and acquisitions.

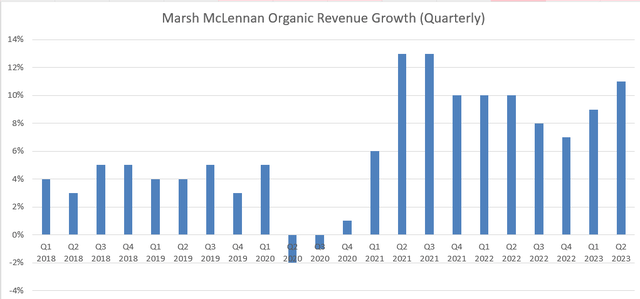

Marsh & McLennan has exhibited robust revenue growth in the post-pandemic era, with their underlying revenue increasing by 11% in Q2 FY23 and adjusted EPS growing by an impressive 16%.

MMC Quarterly Results

They are guiding for high-single-digit underlying revenue growth for FY23 and anticipate continued margin expansion along with strong EPS growth for the full year. This performance indicates that Marsh & McLennan is navigating the current weak economic environment quite effectively.

Key Risks

The Consulting Business, which represents approximately 40% of their total revenue, offers health, wealth, and career solutions to their clients through Mercer and Oliver Wyman Group. Unlike their risk services, the consulting business tends to be more volatile and sensitive to economic conditions. For instance, it experienced a 2% organic decline in FY20. This volatility arises from the project-based nature of the consulting business, where clients may delay or reduce projects in response to budget constraints. Consequently, these business lines carry a somewhat higher level of risk compared to Marsh & McLennan’s other segments, in my assessment.

Valuation

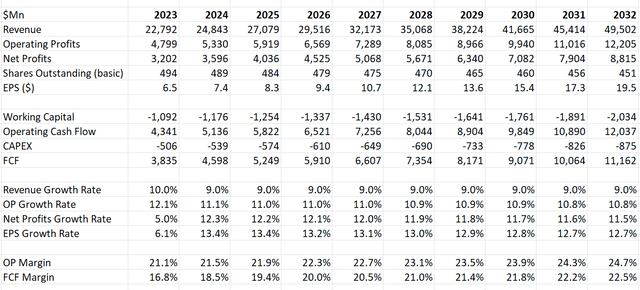

I estimate that Marsh & McLennan will achieve 8% underlying revenue growth in FY23 and 7% in the following years. In addition, M&A is expected to contribute 2% to total revenue growth. Their operating margin is projected to reach 24.7% by FY32, with a free cash margin of 22.5%.

MMC DCF Model – Author’s Calculation

As discussed above, I anticipate that they will persist in making dividend payments, conducting share buybacks, and pursuing acquisitions. Overall, my forecast suggests they will achieve low-to-mid-double-digit earnings growth over the next decade. In my model, I have used a 10% discount rate, a 4% terminal growth rate, and a 25.5% tax rate. After discounting all the free cash flows from the firm and adjusting for their debt and cash balances, the calculated fair value of their stock price is $205 per share.

Conclusions

I believe that Marsh & McLennan is well-managed under the current management team. They are shifting their business mix toward higher-growth areas and actively managing their costs to expand their margins. Considering the valuation, I give MMC stock a ‘Buy’ rating.

{kind=link}